1.项目说明

使用data中的close列的时间序列数据完成预测【使用close列数据中的前windowback-1天数据完成未来一天close的预测】

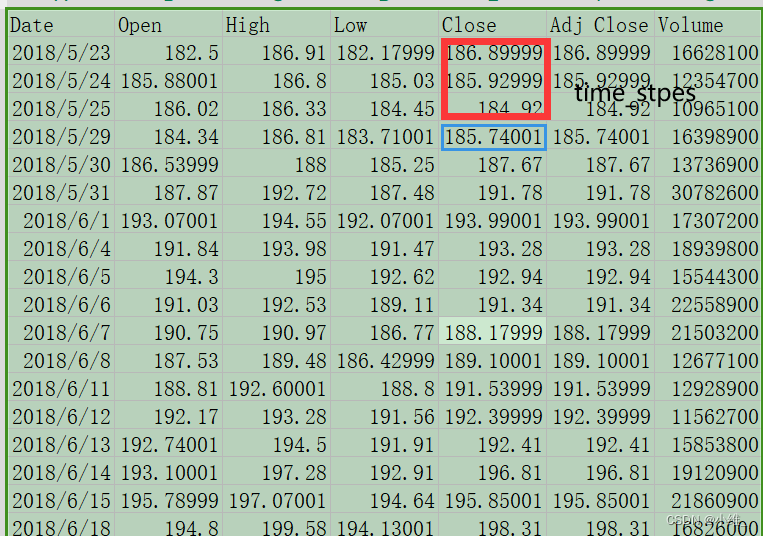

2.数据集

Date,Open,High,Low,Close,Adj Close,Volume

2018-05-23,182.500000,186.910004,182.179993,186.899994,186.899994,16628100

2018-05-24,185.880005,186.800003,185.029999,185.929993,185.929993,12354700

2018-05-25,186.020004,186.330002,184.449997,184.919998,184.919998,10965100

2018-05-29,184.339996,186.809998,183.710007,185.740005,185.740005,16398900

2018-05-30,186.539993,188.000000,185.250000,187.669998,187.669998,13736900

2018-05-31,187.869995,192.720001,187.479996,191.779999,191.779999,30782600

2018-06-01,193.070007,194.550003,192.070007,193.990005,193.990005,17307200

2018-06-04,191.839996,193.979996,191.470001,193.279999,193.279999,18939800

2018-06-05,194.300003,195.000000,192.619995,192.940002,192.940002,15544300

2018-06-06,191.029999,192.529999,189.110001,191.339996,191.339996,22558900

2018-06-07,190.750000,190.970001,186.770004,188.179993,188.179993,21503200

2018-06-08,187.529999,189.479996,186.429993,189.100006,189.100006,12677100

2018-06-11,188.809998,192.600006,188.800003,191.539993,191.539993,12928900

2018-06-12,192.169998,193.279999,191.559998,192.399994,192.399994,11562700

2018-06-13,192.740005,194.500000,191.910004,192.410004,192.410004,15853800

2018-06-14,193.100006,197.279999,192.910004,196.809998,196.809998,19120900

2018-06-15,195.789993,197.070007,194.639999,195.850006,195.850006,21860900

2018-06-18,194.800003,199.580002,194.130005,198.309998,198.309998,16826000

2018-06-19,196.240005,197.960007,193.789993,197.490005,197.490005,19994000

2018-06-20,199.100006,203.550003,198.809998,202.000000,202.000000,28230900

2018-06-21,202.759995,203.389999,200.089996,201.500000,201.500000,19045700

2018-06-22,201.160004,202.240005,199.309998,201.740005,201.740005,17420200

2018-06-25,200.000000,200.000000,193.110001,196.350006,196.350006,25275100

2018-06-26,197.600006,199.100006,196.229996,199.000000,199.000000,17897600

2018-06-27,199.179993,200.750000,195.800003,195.839996,195.839996,18734400

2018-06-28,195.179993,197.339996,193.259995,196.229996,196.229996,18172400

2018-06-29,197.320007,197.600006,193.960007,194.320007,194.320007,15811600

2018-07-02,193.369995,197.449997,192.220001,197.360001,197.360001,13961600

2018-07-03,194.550003,195.399994,192.520004,192.729996,192.729996,13489500

2018-07-05,194.740005,198.649994,194.029999,198.449997,198.449997,19684200

2018-07-06,198.449997,203.639999,197.699997,203.229996,203.229996,19740100

2018-07-09,204.929993,205.800003,202.119995,204.740005,204.740005,18149400

2018-07-10,204.500000,204.910004,202.259995,203.539993,203.539993,13190100

2018-07-11,202.220001,204.500000,201.750000,202.539993,202.539993,12927400

2018-07-12,203.429993,207.080002,203.190002,206.919998,206.919998,15454700

2018-07-13,207.809998,208.429993,206.449997,207.320007,207.320007,11486800

2018-07-16,207.500000,208.720001,206.839996,207.229996,207.229996,11078200

2018-07-17,204.899994,210.460007,204.839996,209.990005,209.990005,15349900

2018-07-18,209.820007,210.990005,208.440002,209.360001,209.360001,15334900

2018-07-19,208.770004,209.990005,207.759995,208.089996,208.089996,11350400

2018-07-20,208.850006,211.500000,208.500000,209.940002,209.940002,16163900

2018-07-23,210.580002,211.619995,208.800003,210.910004,210.910004,16732000

3.数据预处理

3.1 读取数据

ata = pd.read_csv('./data/rlData.csv')

data = data.sort_values('Date')

data.head()

data.shape# 绘制close收盘价和Date时间的二维视图

sns.set_style("darkgrid")

plt.figure(figsize = (15,9))

plt.plot(data[['Close']]) #这里注意输入数据y的数据类型

plt.xticks(range(0,data.shape[0],20), data['Date'].loc[::20], rotation=45)

plt.title("****** Stock Price",fontsize=18, fontweight='bold')

plt.xlabel('Date',fontsize=18)

plt.ylabel('Close Price (USD)',fontsize=18)

plt.show()

3.2 选取特征工程Close列数据

price = data[['Close']]

price.info()

print(price.shape) #(25

3.3 数据归一化

scaler = MinMaxScaler(feature_range=(-1, 1))

price['Close'] = scaler.fit_transform(price['Close'].values.reshape(-1,1))3.4 数据集的制造[batch_size,time_steps,input_size]

def split_data(stock, lookback):data_raw = stock.to_numpy() data = [] # you can free play(seq_length)for index in range(len(data_raw) - lookback): #这里input的shape[252,1],然后每次取input中的[]"""input= [[1],[2]...[252]] input.shape=[252,1] 每次循环取input[i:i+lookback],[[1],[2]...[lookback]] shape=[3,1]然后存到data列表中,经过若干次循环后就变成了【len(data_raw)-lookback,3,1】"""data.append(data_raw[index: index + lookback])data = np.array(data)# print(data_raw.shape) #(252, 1)# print(data.shape) #(249, 3, 1)test_set_size = int(np.round(0.2 * data.shape[0]))train_set_size = data.shape[0] - (test_set_size)x_train = data[:train_set_size,:-1,:] #当lookback=n时,本代码表示将time_step=n-1,其他数据不变y_train = data[:train_set_size,-1,:] #当lookback=n时,本代码表示将n-1个数据作为y,且数据shape也会不变,和x_train保持一直x_test = data[train_set_size:,:-1,:]y_test = data[train_set_size:,-1,:]return [torch.Tensor(x_train), torch.Tensor(y_train), torch.Tensor(x_test),torch.Tensor(y_test)]lookback = 3

x_train, y_train, x_test, y_test = split_data(price, lookback)

print('x_train.shape = ',x_train.shape) #(199, 2, 1)

print('y_train.shape = ',y_train.shape)

print('x_test.shape = ',x_test.shape) #x_test.shape = (50, 2, 1)

print('y_test.shape = ',y_test.shape)

4.LSTM算法

class LSTM(nn.Module):def __init__(self, input_dim, hidden_dim, num_layers, output_dim):super(LSTM, self).__init__()self.hidden_dim = hidden_dimself.num_layers = num_layersself.lstm = nn.LSTM(input_dim, hidden_dim, num_layers, batch_first=True)self.fc = nn.Linear(hidden_dim, output_dim)def forward(self, x):"""batch_first=True:则输入为x.shape = (batch_size,time_steps,input_size)out.shape = (batch_size,time-steps,ouput_size)"""h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()# x.shape = (batch_size,time_steps,input_size)# out.shape = (batch_size,time_steps,ouput_size)out, (hn, cn) = self.lstm(x, (h0.detach(), c0.detach()))#out.shape是选取time_steps列的最后一个数据 out.shape = (batch_size,ouput_size)out = self.fc(out[:, -1, :]) return out

5.预训练

input_dim = 1

hidden_dim = 32

num_layers = 2

output_dim = 1

num_epochs = 100model = LSTM(input_dim=input_dim, hidden_dim=hidden_dim, output_dim=output_dim, num_layers=num_layers)

criterion = torch.nn.MSELoss()

optimiser = torch.optim.Adam(model.parameters(), lr=0.01)hist = np.zeros(num_epochs)

lstm = []for t in range(num_epochs):#x_train.shape=torch.Size([199, 2, 1]) [batch_size,time_steps,input_size]#y_train_pred.shape=torch.Size([199, 1]) [batch_size,ouput_size]y_train_pred = model(x_train) loss = criterion(y_train_pred, y_train_lstm)# print("Epoch ", t, "MSE: ", loss.item())hist[t] = loss.item()optimiser.zero_grad()loss.backward()optimiser.step()

6.绘制预测值和真实值拟合图形,以及loss图形

#绘制预测值y_train_pred和真实值y_train二维视图

predict = pd.DataFrame(scaler.inverse_transform(y_train_pred.detach().numpy()))

original = pd.DataFrame(scaler.inverse_transform(y_train.detach().numpy()))sns.set_style("darkgrid")

fig = plt.figure()

fig.subplots_adjust(hspace=0.2, wspace=0.2)plt.subplot(1, 2, 1)

ax = sns.lineplot(x = original.index, y = original[0], label="Data", color='royalblue')

ax = sns.lineplot(x = predict.index, y = predict[0], label="Training Prediction (LSTM)", color='tomato')

ax.set_title('Stock price', size = 14, fontweight='bold')

ax.set_xlabel("Days", size = 14)

ax.set_ylabel("Cost (USD)", size = 14)

ax.set_xticklabels('', size=10)plt.subplot(1, 2, 2)

ax = sns.lineplot(data=hist, color='royalblue')

ax.set_xlabel("Epoch", size = 14)

ax.set_ylabel("Loss", size = 14)

ax.set_title("Training Loss", size = 14, fontweight='bold')

fig.set_figheight(6)

fig.set_figwidth(16)7.测试集测试

model.eval()# make predictions

y_test_pred = model(x_test)# invert predictions

y_train_pred = scaler.inverse_transform(y_train_pred.detach().numpy())

y_train = scaler.inverse_transform(y_train.detach().numpy())

y_test_pred = scaler.inverse_transform(y_test_pred.detach().numpy())

y_test = scaler.inverse_transform(y_test.detach().numpy())# calculate root mean squared error

trainScore = math.sqrt(mean_squared_error(y_train[:,0], y_train_pred[:,0]))

print('Train Score: %.2f RMSE' % (trainScore))

testScore = math.sqrt(mean_squared_error(y_test[:,0], y_test_pred[:,0]))

print('Test Score: %.2f RMSE' % (testScore))

lstm.append(trainScore)

lstm.append(testScore)

lstm.append(training_time)完整代码

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.preprocessing import MinMaxScaler

import torch

import torch.nn as nn

import time

import math, time

from sklearn.metrics import mean_squared_error

import seaborn as snsdata = pd.read_csv('./data/rlData.csv')

data = data.sort_values('Date')

data.head()

data.shape# 绘制close收盘价和Date时间的二维视图

sns.set_style("darkgrid")

plt.figure(figsize = (15,9))

plt.plot(data[['Close']]) #这里注意输入数据y的数据类型

plt.xticks(range(0,data.shape[0],20), data['Date'].loc[::20], rotation=45)

plt.title("****** Stock Price",fontsize=18, fontweight='bold')

plt.xlabel('Date',fontsize=18)

plt.ylabel('Close Price (USD)',fontsize=18)

plt.show()#1.选取特征工程Close类数据

price = data[['Close']]

price.info()

print(price.shape) #(252, 1)#2.数据归一化

scaler = MinMaxScaler(feature_range=(-1, 1))

price['Close'] = scaler.fit_transform(price['Close'].values.reshape(-1,1))#3.数据集的制作

def split_data(stock, lookback):data_raw = stock.to_numpy() data = [] # you can free play(seq_length)for index in range(len(data_raw) - lookback): #这里input的shape[252,1],然后每次取input中的[]"""input= [[1],[2]...[252]] input.shape=[252,1] 每次循环取input[i:i+lookback],[[1],[2]...[lookback]] shape=[3,1]然后存到data列表中,经过若干次循环后就变成了【len(data_raw)-lookback,3,1】"""data.append(data_raw[index: index + lookback])data = np.array(data)# print(data_raw.shape) #(252, 1)# print(data.shape) #(249, 3, 1)test_set_size = int(np.round(0.2 * data.shape[0]))train_set_size = data.shape[0] - (test_set_size)x_train = data[:train_set_size,:-1,:] #当lookback=n时,本代码表示将time_step=n-1,其他数据不变y_train = data[:train_set_size,-1,:] #当lookback=n时,本代码表示将n-1个数据作为y,且数据shape也会不变,和x_train保持一直x_test = data[train_set_size:,:-1,:]y_test = data[train_set_size:,-1,:]return [torch.Tensor(x_train), torch.Tensor(y_train), torch.Tensor(x_test),torch.Tensor(y_test)]lookback = 3

x_train, y_train, x_test, y_test = split_data(price, lookback)

print('x_train.shape = ',x_train.shape) #(199, 2, 1)

print('y_train.shape = ',y_train.shape)

print('x_test.shape = ',x_test.shape) #x_test.shape = (50, 2, 1)

print('y_test.shape = ',y_test.shape)class LSTM(nn.Module):def __init__(self, input_dim, hidden_dim, num_layers, output_dim):super(LSTM, self).__init__()self.hidden_dim = hidden_dimself.num_layers = num_layersself.lstm = nn.LSTM(input_dim, hidden_dim, num_layers, batch_first=True)self.fc = nn.Linear(hidden_dim, output_dim)def forward(self, x):"""batch_first=True:则输入为x.shape = (batch_size,time_steps,input_size)out.shape = (batch_size,time-steps,ouput_size)"""h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()# x.shape = (batch_size,time_steps,input_size)# out.shape = (batch_size,time_steps,ouput_size)out, (hn, cn) = self.lstm(x, (h0.detach(), c0.detach()))#out.shape是选取time_steps列的最后一个数据 out.shape = (batch_size,ouput_size)out = self.fc(out[:, -1, :]) return outinput_dim = 1

hidden_dim = 32

num_layers = 2

output_dim = 1

num_epochs = 100model = LSTM(input_dim=input_dim, hidden_dim=hidden_dim, output_dim=output_dim, num_layers=num_layers)

criterion = torch.nn.MSELoss()

optimiser = torch.optim.Adam(model.parameters(), lr=0.01)hist = np.zeros(num_epochs)

lstm = []for t in range(num_epochs):#x_train.shape=torch.Size([199, 2, 1]) [batch_size,time_steps,input_size]#y_train_pred.shape=torch.Size([199, 1]) [batch_size,ouput_size]y_train_pred = model(x_train) loss = criterion(y_train_pred, y_train_lstm)# print("Epoch ", t, "MSE: ", loss.item())hist[t] = loss.item()optimiser.zero_grad()loss.backward()optimiser.step()#绘制预测值y_train_pred和真实值y_train二维视图

predict = pd.DataFrame(scaler.inverse_transform(y_train_pred.detach().numpy()))

original = pd.DataFrame(scaler.inverse_transform(y_train.detach().numpy()))sns.set_style("darkgrid")

fig = plt.figure()

fig.subplots_adjust(hspace=0.2, wspace=0.2)plt.subplot(1, 2, 1)

ax = sns.lineplot(x = original.index, y = original[0], label="Data", color='royalblue')

ax = sns.lineplot(x = predict.index, y = predict[0], label="Training Prediction (LSTM)", color='tomato')

ax.set_title('Stock price', size = 14, fontweight='bold')

ax.set_xlabel("Days", size = 14)

ax.set_ylabel("Cost (USD)", size = 14)

ax.set_xticklabels('', size=10)plt.subplot(1, 2, 2)

ax = sns.lineplot(data=hist, color='royalblue')

ax.set_xlabel("Epoch", size = 14)

ax.set_ylabel("Loss", size = 14)

ax.set_title("Training Loss", size = 14, fontweight='bold')

fig.set_figheight(6)

fig.set_figwidth(16)# 设置成eval模式

model.eval()# make predictions

y_test_pred = model(x_test)# invert predictions

y_train_pred = scaler.inverse_transform(y_train_pred.detach().numpy())

y_train = scaler.inverse_transform(y_train.detach().numpy())

y_test_pred = scaler.inverse_transform(y_test_pred.detach().numpy())

y_test = scaler.inverse_transform(y_test.detach().numpy())# calculate root mean squared error

trainScore = math.sqrt(mean_squared_error(y_train[:,0], y_train_pred[:,0]))

print('Train Score: %.2f RMSE' % (trainScore))

testScore = math.sqrt(mean_squared_error(y_test[:,0], y_test_pred[:,0]))

print('Test Score: %.2f RMSE' % (testScore))

lstm.append(trainScore)

lstm.append(testScore)

lstm.append(training_time)

参考:https://gitee.com/qiangchen_sh/stock-prediction/blob/master/%E4%BB%A3%E7%A0%81/LSTM%E4%BB%8E%E7%90%86%E8%AE%BA%E5%9F%BA%E7%A1%80%E5%88%B0%E4%BB%A3%E7%A0%81%E5%AE%9E%E6%88%98%203%20%E8%82%A1%E7%A5%A8%E4%BB%B7%E6%A0%BC%E9%A2%84%E6%B5%8B_Pytorch.ipynb#